Off-Grid Resources

The resources on this page provide valuable market intelligence for off-grid energy stakeholders, including Off-Grid Solar Market Assessments, a Financial Modeling Tool for PAYGO Energy Access Companies, a collection of Off-grid Productive Use of Energy Catalogs, and Additional Resources.

OFF-GRID SOLAR MARKET ASSESSMENTS

These reports by Power Africa provide insights into the opportunities and risks associated off-grid solar energy markets in various countries and gives companies, investors, governments, and other stakeholders a deeper understanding of the market.

While there are other market assessments conducted by other stakeholders (i.e. development partners), Power Africa recognizes a gap in the available market assessments. Bridging the gap, these reports are characterized by the following:

- These reports provide comprehensive and detailed reviews of solar home systems (SHSs), mini-grids, productive use of energy, and other aspects of the off-grid solar value chain. Additionally, this report includes details on policy and regulatory issues, the structure and historical context of the energy sector, and gender mainstreaming.

- These reports draw upon the most up-to-date sales and investment data from the Global Off-Grid Lighting Association (GOGLA) in order to keep pace with the ever-changing dynamics of the off-grid solar sector. They also include geospatial analysis that highlights potential areas for off-grid solar market expansion.

- Insights in these reports help Power Africa and other stakeholders plan and prioritize activities across work streams of policy and regulations, market intelligence, business performance, access to finance, and cross-sectoral integration throughout sub-Saharan Africa.

- Supplemental Productive Use of Energy (PUE) Assessments in some markets detail available technologies, stakeholders involved in the PUE supply chain, opportunities for new PUE technologies, and potential for off-grid energy companies to provide PUE solutions.

These reports also serve as a baseline for Power Africa’s technical advisors to guide their continuing work and provide a snapshot that can be used to determine growth and changing dynamics of the markets over time. Insights provided in these reports include characteristics of a country's electricity sector, electrification targets, government regulations, donor-funded activities, and details on subsectors of the off-grid solar energy market. Additionally, these reports include expert knowledge from Power Africa lead advisors, information gathered from stakeholder interviews, and data from GOGLA.

To jump to a report, click on the country name in the list below:

Cameroon

Cameroon is a Central African state, approximately 475,442 square kilometers (km2) in size, with a coastline on the Gulf of Guinea of approximately 420 kilometers. Its population is approximately 23 million people, 56 percent of whom live in urban areas. Life expectancy is 58 years. The population density is 49 people per km2, and the country’s annual population growth is 2.6 percent. Cameroon’s key economic indicators include:

- The gross domestic product was approximately $34 million in 2017, with a growth rate of 3.5 percent and a per capita income of $1,447.

- Cameroon’s main exports are aluminum, bananas, cocoa beans, coffee, cotton, petroleum, palm oil, rubber, and wood.

- The main employment sector in Cameroon is agriculture, which employs 60 percent of the country’s workforce, of which approximately 60 percent are women and 40 percent are men.

Cameroon’s Vision 2035 outlines the country’s development policy goals. However, the country must overcome several challenges on the way, as it faces unprecedented violence in the Northwest and Southwest Regions, where thousands of internally displaced persons are registered. The economy is at a standstill in these regions and social conditions have completely degraded.

Côte d’Ivoire

Côte d’Ivoire - the world’s largest producer of cocoa and cashew nuts, a net oil exporter, with a rapidly growing manufacturing sector - has enjoyed remarkable economic success since 2012 and is a major economic power in the West Africa region.1 However, Côte d’Ivoire is still challenged by issues of poverty, financial inclusion and literacy, inequitable distribution of wealth, and universal access to goods and services that are required for a modern economy, including reliable and affordable electricity. To understand Côte d’Ivoire in broad terms, the following points are key:

- In 2015, approximately 46.3 percent of the population lived below the poverty line. Despite recent economic growth, wealth is not equitably distributed.

- In 2017, the Gross Domestic Product (GDP) was approximately $37 billion, which is anticipated to grow annually by more than 7 percent during the next 5 years. Continued economic growth will put additional demands on an already strained national grid.

- In 2018, the estimated population was 24 million residents, with approximately 50.8 percent living in urban areas; however only approximately 64 percent of residents have access to electricity, irrespective of reliability.

- In Côte d’Ivoire, 49.3 percent of men and 45.4 percent of women are self-employed in agriculture, making agriculture perhaps the most important sector to the health the country’s economy. Electricity access can provide substantial productivity gains to one of Côte d’Ivoire’s most important sectors.

- Côte d’Ivoire is the world’s largest exporter of unprocessed cocoa beans. Off-grid productive use of energy for agriculture, including processing cocoa beans, could increase economic activity in Côte d’Ivoire, thereby increasing economic growth and rural development.

Democratic Republic of the Congo

DRC is the fourth most populated country in Africa with an estimated population of 85.8 million people. Approximately 12 million people live in the capital Kinshasa. The remaining population is spread out throughout the country at a low density of 38 people per square kilometer. The growth rate of its population is three percent per year. Currently, more than 40 percent of the population lives in urban areas. Despite a recent period of economic growth, including growth within the energy sector, DRC is still one of the poorest and least developed countries in Africa and has active conflict zones.

Ethiopia

Ethiopia is Africa’s oldest independent country and its second largest in terms of population, while also being one of the poorest countries in Africa. The Government of Ethiopia (GOE) is currently implementing the second phase of its Growth and Transformation Plan II (GTP II), which aims for Ethiopia to achieve lower middle income and carbon-neutral status by 2025.1 Along with Ethiopia’s ambitious poverty reduction strategies and targets, the government has recently released its National Electrification Plan 2.0 (NEP 2.0), which strives for universal electrification by 2025 through a mix of on- and off-grid energy solutions. The following statistics provide insight into Ethiopia’s country context:

- Gross domestic product (GDP) in 2018 was $84.4 billion, with an average per capita income of $772.

- In 2018, the estimated population was approximately 109 million people, with more than 80 percent living in rural areas.

- From 2011 to 2016, poverty dropped by 20 percent in Ethiopia. However, poverty in rural areas increased during the same time frame.

- Over 15 languages are spoken in Ethiopia, the primary languages are Oromo and Amharic.

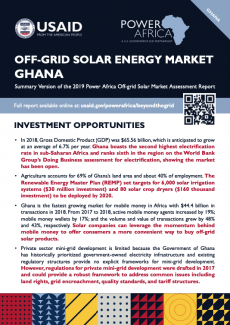

Ghana

Ghana’s off-grid power sector is characterized by government policies and donor-funded projects that stress government ownership of energy assets. It is also shaped by private solar home systems (SHS) companies that directly serve consumers. Both government- and company-led approaches are complicated by Ghana’s high, 84 percent, nation electrification rate,1 as remaining off-grid communities present challenges regarding the distribution, installation, and/or servicing of systems.

Government electrification efforts are guided by the Rural Electrification Master Plan, which is a highlevel planning document that sets deployment targets for stand-alone solar systems, solar lanterns, and mini-grids. The implementation of electrification projects is typically funded by donors, such as the African Development Bank’s (AfDB) Ghana Scaling up Renewable Energy Program.

Kenya

Kenya is a country with an area of 569,000 square kilometers and has a population of close to 50 million people. The main languages are Swahili and English (both official). 1 Several ethnic languages are also spoken in the country. Two of the most widely spoken languages are Kikuyu and Luhya, but other languages include Luo, Kalenjin, Kamba, and Mijikenda. The total number of languages spoken is estimated at 68.

Kenya has the largest and most dynamic economy in East Africa, with a gross domestic product (GDP) of $85 billion (KSh8,904,983.9M, 2018) with a growth rate averaging 5.6 percent year-on-year over the past 5 years. 3 Major industries include agriculture, forestry, fishing, mining, manufacturing, energy, tourism, and financial services. In its development plans, the Government of Kenya (GoK) aspires to become a newly industrializing middle-income country by 2030.4 Kenya is implementing Vision 2030 through five-year medium-term plans. The current plan for 2018–2022 focuses on four agenda items (referred to as the Big Four Agenda): universal healthcare, affordable housing, food security, and manufacturing. The success of the Big Four Agenda depends on adequate, affordable, and reliable electricity.

Liberia

Liberia is a West African country with a population of nearly five million. Poverty is widespread with 41 percent of the population living on less than $ 1.90 per day.

Liberia has one of the lowest rates of electrification in the world. Roughly 17 percent of the urban population and 2 percent of the rural population have access to electricity. Liberia experienced civil conflict from 1985-2003, which damaged 75 percent of the road and electrical infrastructure. Since 2003, Liberia has been working to rebuild its infrastructure.

In line with the Sustainable Development Goals (SDGs), Liberia is working to attain 70 percent electrification of the capital city and 35 percent of rural areas by 2030, but much remains to be done, particularly in rural regions.

Niger

The Republic of Niger (Niger) is a nation of nearly 21.5 million people in West Africa (Table ES-1). The population of Niger is predominantly rural and reliant on subsistence agriculture; 96 percent of the population is clustered in the southernmost regions of Dosso, Maradi, Tahoua, Tillabéri, and Zinder, which represent only 35 percent of the land area. This concentration is the result of the more hospitable climate of the southernmost regions and the proximity to Nigeria, a key economic partner.

Rwanda

Rwanda has made substantial progress towards its goal in energy access, moving from 6 percent on-grid access in 2000 to 37 percent on-grid access in 2019. Despite this impressive progress, the low starting point represents an opportunity for the off-grid sector to flourish. It has already reached 14 percent of the population. These numbers indicate that although other countries may have larger markets in terms of absolute size, the impacts of the off-grid sector within the overall energy sector are very high in Rwanda. The Government of Rwanda (GOR) has also shown its commitment to the off-grid sector by setting a target for 48 percent of the population to be served by an off-grid product by 2024.

To date, small solar home systems (SHSs), sold through a pay-as-you-go (PAYG) model, have dominated the off-grid sector, which is a situation similar to other markets in East Africa. However, according to results from the Fifth Integrated Household Living Conditions Survey (EICV5), the ability to pay is low in Rwanda. The survey shows that 75 percent of off-grid households spent less $1.67 per month on lighting and telephone charging. This constraint has been recognized by GOR, which is working with development partners to design a subsidy.

Senegal

Senegal is home to one of West Africa’s leading off-grid power sectors. The country’s private-sector solar home system (SHS) companies have been at the forefront of adopting proven business models and technologies from East Africa, while also innovating through partnerships with microfinance institutions. Contributing to Senegal’s position as a regional leader are a relatively strong human resource pool and good transportation links to neighboring countries. Professionals in Senegal are experienced in business and have networks spanning the region.

At the same time, government policies, originally developed in the late 1990s, have provided an official framework for private development and financing of large-scale grid infrastructure, mini-grids, and standalone power systems. Although this framework has not entirely delivered on expected results, it has helped to attract large quantities of donor finance.

Tanzania

Tanzania is the sixth most populous country in sub-Saharan Africa. It connects six land-locked countries to the Indian Ocean and has deep natural gas reserves, and there are many opportunities for investment.

Tanzania has abundant and world-class wind and solar resources. The Government of Tanzania (GOT) has committed to reform the operations of the Tanzania Electric Supply Company Ltd. (TANESCO, the national utility) and meet new demand through low-cost solutions.

High reliance on expensive thermal and emergency generation sources have helped make the sector financially unviable. The following statistics provide insight into the Tanzanian country context:

- In 2017, the gross domestic product was $52.09 billion, with a growth rates of nearly seven percent over the past decade.

- In 2018, the population was approximately 56 million people, with approximately 67 percent living in rural areas.

- In 2016 (the most recent data available according to the World Bank), 26.8 percent of the population lived below the poverty line in Tanzania.

- There are more than 120 ethnic groups in Tanzania, with as many languages, and the official languages are English and Swahili.

Uganda

Uganda is a landlocked country in East Africa, with a gross domestic product worth $36 billion in 2020 and a projected growth-rate of 6.63 percent. Uganda’s population stands at 41 million, with 27 percent living in urban areas. Uganda has one of the youngest and most rapidly growing populations in the world: 54 percent of the population is younger than 18. The government of Uganda expects rapid population growth along with demand for jobs, housing, health, and energy, presenting great potential for renewable energy, particularly off-grid solar, to be adopted rapidly.

Sixty-eight percent of Ugandans work in agriculture. Trading employs 10.4 percent of the population and manufacturing four percent. Uganda is richly endowed with natural resources, including large deposits of crude oil, vast forests, large bodies of water, natural hot springs, precious minerals, and year-round sunshine, with the total renewable energy potential estimated at 5.3 GW, of which only 1,364.6 MW had been installed in 2021.

OFF-GRID PRODUCTIVE USE OF ENERGY CATALOGS

The main objective of Power Africa's off-grid productive use of energy (PUE) catalogs is to increase awareness and uptake of off-grid PUE appliances available in the sub-Saharan African market for agriculture, fishing, livestock, and poultry. The catalogs provide stakeholders – including manufacturers, suppliers, non-government and community organizations, and government policymakers – with insight into PUE products and innovations.

The catalogs include:

- Product technical specifications

- Manufacturer information

- Distribution channels

- Local distributor details

- Product payment methods and pay as you go integration capabilities

- Quality standards

- Links to related sources

ADDITIONAL OFF-GRID MARKET RESOURCES

Business Development

- Distribution Partnership Tool - Developing the Route to Market: A Tool for Expanding Off-Grid Solar Product Distribution

- PAYGO Guide for Off-grid Energy Companies

- Microfinance Loans for Increasing Access to Off-Grid Solar Products Guide

- PAYGO Credit Risk Management Guide

- Sales Training Materials for Off-Grid-Solar Companies

- Off-Grid Energy Access Learning Guide for Southern Africa

- White Paper: Carbon Credits for Off-grid Solar in Sub-Saharan Africa - Lessons from Energy-access Companies in the Voluntary Carbon-credit Market

- Learning Paper: Helping Off-grid Companies Enhance Credit-risk Management Practices - From PAYGO 1.0 to PAYGO 2.0

- Financial Management Handbook for Off-Grid Solar Companies - Lessons on Financial Management from Tailored Support

- Demystifying Securitization for Off-grid Companies

Gender

- Case Study: Gender Smart Investing

- Case Study Ghana: Advancing Gender Equality in Africa's Off-grid Energy Sector (English)

- Case Study Ghana: Advancing Gender Equality in Africa's Off-grid Energy Sector (French)

- Reaching Women, Unlocking Value: How Gender Inclusivity Boosts Customer Satisfaction for Off-Grid Solar Products

- Gender Inclusion Assessment Tool for Off-grid Energy Companies

- Outil d'Évaluation de l'Inclusion du Genre Pour les Entreprises d'Énergie Hors Réseau

- Increasing Women’s Access to Off-Grid Productive Use of Energy for Agriculture:

Kenya

- Off-grid Solar Market Assessment Report for 14 Underserved Counties of Kenya

This report:

- Quantifies and characterizes the off-grid population in underserved areas

- Identifies individual off-grid settlements

- Scores settlements for off-grid suitability

- Comprises valuable market insight to inform service delivery

Malawi

- Malawi Route-to-Market Geospatial Tool Document Release

- Malawi Route-to-Market Tool Training Video Document Release

- Malawi Route-to-Market Tool Training Video

- Malawi RTM Tool Tutorial Part 1: Welcome and Introduction

- Malawi RTM Tool Tutorial Part 2: Overview and Approach: Section 2 – Tools

Mozambique

- Can Mozambican Households Afford SHS? Insights From A Local Survey

- Mozambique Route-to-Market Tool (UPDATED - Version 6 available)

Nigeria

- Sector Financial Assessment

- Legal and Enabling Environment

- Off-Grid Assessment

- Agricultural Productive Use Stimulation in Nigeria: Value Chain and Mini-Grid Feasibility Study

- Productive Use Cold Storage Systems Report

- Productive Use Solar Irrigation Systems in Nigeria

- Market Intelligent Report 2021

Off-grid Clean Energy Financial Modeling Bootcamp Self-study Material & Videos

Rwanda

Uganda

- De-Risking Pay-As-You-Go Solar Home Systems in Uganda Refugee Settlement Project Report

- Advancing Energy Access in Refugee Settlements (infographic of above project report)

Zambia

ENERGY FORESHIGHT REPORT

Off-Grid Energy in 2030 - An Exercise in Foresighting

What will the off-grid energy landscape in sub-Saharan Africa look like in 2030?

Our foresight report looks toward the year 2030, investigating the opportunities for off-grid energy. Focusing on drivers of change and signals of innovation, the report explores potential futures for the intersection of off-grid power and:

- Climate change

- Digital finance

- Gender equality

- Electric mobility

FINANCIAL MODELING TOOL FOR PAYGO ENERGY ACCESS COMPANIES

The Financial Modeling Tool for Pay-as-you-go (PAYGO) Energy Access companies:

- Guides internal financial management processes

- Enables projections of company financials based on different scenarios

- Introduces methods that can guide company valuation

- Models key aspects of PAYGO companies

DOWNLOAD

- 2021 Financial Modeling Tool - User Guide

- 2021 PAYGO Financial Modeling Tool

- 2021 PAYGO Financial Modeling Tool - With Sample Input - Financial modeling tool with sample input to demonstrate dashboard functionality

- 2021 PAYGO Simplified Business Model - Simplified presentation of the PAYGO business model (“back of the envelope” calculation which can be used to explain the business model to a third party, typically an investor, in a way that is easy to understand)

- 2021 PAYGO Financial Modeling Tool - Additional Products Sheet - A complementary worksheet for additional products (for companies offering multiple product lines)

- Supporting Off-grid Solar Startups with Financial Modeling: 12 Lessons

VIEW

Disclaimer

The Financial Modeling Tool for PAYGO Energy Access Companies (the Tool) is intended for use by companies evaluating pay-as-you-go (PAYGO) technology and business models. The Tool is designed primarily for solar home system (SHS) and productive use of energy companies. The Tool is designed for illustrative use in connection with internal financial management processes, such as liquidity management, unit economics analysis, and forecasting. The Tool is provided to the public in good faith and based on the objectives stated above and is not to be sold by third parties. The Tool is not comprehensive. USAID does not make any representations or warranties (expressed or implied) as to the accuracy or completeness of the Tool. Users of the Tool should neither treat nor rely on the contents and calculations of the Tool as advice relating to legal, taxation, investment, accounting, or other matters and are advised to consult professional advisors in those areas. Interested parties should conduct their own inquiries, investigation, and analysis of the information set forth in the Tool. The Tool may include forward-looking statements that represent opinions, expectations, beliefs, intentions, estimates, or strategies regarding the future, which may not be realized. Actual and future results and trends could differ materially from those described by such statements and from projections made by the Tool. To the fullest extent permitted by law, USAID and Power Africa shall have no liability whatsoever to the user or any third party, with regard to the usage of the Tool, output of the Tool, or decisions made based upon the Tool, including the accuracy or completeness thereof. USAID and Power Africa expressly disclaim any and all legal responsibility and liability that may be based on the use of, or information provided by, the Tool or errors or omissions therein. Use of the Tool should not be construed as an endorsement by the U.S. Government of any particular company, possible investment, technology or business model. USAID did not verify the accuracy of any information derived from public sources. USAID may update, replace or withdraw the Tool or the information contained herein, in part or entirely, at any time, and undertakes no obligation to notify users.